[Editor's Note: The public comment period ended February 10, 2023.]

The US Department of Education is accepting public comments as a Request for Information (RFI) about "Public Transparency for Low-Financial-Value Postsecondary Programs." The announcement is available at the US Federal Register.

As with most US government rules and policies, industry insiders have great influence in these decisions--and concerned citizens are often shut out of the process. When consumers do have a chance to speak, they may not even know of those opportunities. That's why the Higher Education Inquirer is asking student loan debtors to contribute to this RFI while they can.

Tell DC policymakers and technocrats about your unique struggles (and your family's struggles) tied to student debt--and what could be done to better inform consumers like you.

There you can find public comments that have already been made. As of February 15, only 129 comments were posted.

According to the announcement:

"a misalignment of prices charged to financial benefits received may cause particularly acute harm for student loan borrowers who may struggle to repay their debts after discovering too late that their postsecondary programs did not adequately prepare them for the workforce. Taxpayers also shoulder the costs when a substantial number and share of borrowers are unable to successfully repay their loans. The number of borrowers facing challenges related to the repayment of their student loans is significant."

The Request for Information continues...

"Programs that result in students taking on excessive amounts of debt can make it challenging for students to reach significant life milestones like purchasing a home, starting a family, or saving enough for retirement, ultimately undermining their ability to climb the economic mobility ladder. Especially for borrowers who attended graduate programs, debt-to-income ratios often rise well above sustainable levels. IDR (Income-Driven Repayment) plans also cannot fully protect borrowers from the consequences of low financial-value programs. For instance, IDR plans cannot give students back the time they invested in such programs. For many programs, the cost of students' time may be at least as significant as direct program costs such as tuition, fees, and supplies. Loans will also still show up on borrowers' credit reports, including any periods of delinquency or default prior to enrollment in IDR."

"The Biden-Harris Administration is committed to improving accountability for institutions of higher education. One component of that work is to increase transparency and public accountability by drawing attention to the postsecondary programs that are most likely to leave students with unaffordable loans and provide the lowest financial returns for students and taxpayers."

CECU, an group representing for-profit colleges, has an organized effort to protect its interests.

Meanwhile, Robert Kelchen has provided an EXCEL spreadsheet that provides many answers. The dataset covers 45,971 programs at 5,033 institutions with data on both student debt and earnings for those same cohorts. We found more than 12,200 programs where debt exceeds income. And more than 7200 programs resulted in median incomes of less than $25,000 a year with debt greater than $10,000.

While some of these high-debt programs in medicine and law may eventually be profitable, many more paint a picture of struggle with a lifetime of debt peonage. Cosmetology schools had a large number of low-income programs. But the fine arts, humanities, social sciences, and education also produced low-value programs in terms of debt to income ratio.

Some of subprime schools HEI has been investigating (Purdue University Global, University of Arizona Global, The Art Institutes) had a number of low-value majors. But elite and brand name schools like Duke, Drexel, Emory, Syracuse, Baylor, DePaul, New School, and University of Rochester even have high debt and low-income programs.

The Congressional Budget Office (CBO) has dramatically revised its projections for the federal student loan program, transforming what was once expected to be a profitable government investment into a significant fiscal liability. This report examines the details of these projection changes and analyzes the operational costs of the Federal Student Aid (FSA) program.

The CBO's updated budget projections released in 2024 reveal a stark shift in the expected financial performance of the federal student loan program. These projections represent a significant revision from earlier expectations and highlight growing concerns about the sustainability of current student lending policies.

According to the Committee for a Responsible Federal Budget (CRFB), the estimated federal cost of student loans issued between 2015 and 2024 has increased by $340 billion – transforming from a projected gain of $135 billion in the 2014 baseline to an expected loss of $205 billion in the 2024 baseline15. This represents a complete reversal in the financial outlook for the program over the past decade.

This dramatic shift is particularly evident when examining the changing projections for specific loan cohorts. In 2014, the CBO projected that taxpayers would generate an 11-cent profit for every dollar of student loans issued by the federal government in fiscal year 2024. However, the most recent projections indicate that taxpayers will instead incur a 20-cent loss per dollar of loans issued this fiscal year6.

Looking ahead, the situation appears even more concerning. Over the 2024-2034 budget window, the CBO expects federal student loans to cost taxpayers $393 billion1. This amount exceeds the $355 billion CBO expects to be spent on Pell Grants, the flagship college aid program for low-income students, over the same time period1.

The projected $393 billion cost includes several components:

$221 billion in losses on the $1.1 trillion in student loans the federal government will issue during this period

$140 billion in re-estimates of the losses taxpayers will bear on outstanding loans

$34 billion toward administering the student loan programs6

One particularly concerning aspect of the CBO projections is the growing cost of graduate student loans. These loans are expected to make up around half of new student loans originated in the current fiscal year11. The CBO projects that taxpayers will lose $102 billion on lending to graduate students over the coming decade11. According to the CRFB, graduate school loans are now nearly as subsidized as undergraduate loans and make up half of the cost of newly issued student loans15.

The dramatic increase in projected costs has several primary causes, as identified in the CBO reports and analyses by financial experts.

The primary catalyst for the growing losses is the expansion and increased utilization of income-driven repayment (IDR) plans6. While a borrower repaying loans under a traditional fixed-term repayment plan typically repays more than the initial amount borrowed, a typical borrower using an IDR plan will repay significantly less than the original loan amount6.

The CBO projects that taxpayers will lose between 30 and 48 cents for every dollar in federal student loans issued in fiscal year 2024 and repaid on an IDR plan1. Preston Cooper notes in his LinkedIn post that "the role of IDR plans in driving these costs can't be overstated. CBO generally expects taxpayers to profit on loans repaid through traditional fixed-term repayment plans. But loans repaid on IDR plans will incur losses ranging from 30 to 48 cents on the dollar"1.

The Biden administration's student loan forgiveness initiatives are cited as significant contributors to the growing cost of the program. The House Budget Committee press release states that "$140 billion or over a third of this cost directly stems from President Biden's student loan forgiveness schemes"7. These initiatives include changes to income-driven repayment plans to make them more generous1.

Beyond the projected losses on the loans themselves, the Federal Student Aid (FSA) program incurs significant operational costs to administer federal student aid programs.

According to FSA's 2024 annual report, the agency operated on an annual administrative budget of approximately $2.1 billion during FY 20244. As of September 30, 2024, FSA was staffed by 1,444 full-time employees who are primarily based in FSA's headquarters in Washington, DC, with additional staff in 10 regional offices throughout the country4.

The Department of Education's Salaries and Expenses Overview provides additional insight into how these administrative funds are allocated. The Student Aid Administration account consists of two primary components:

Salaries and Expenses

Servicing Activities

In the fiscal year 2020 budget request, for example, the Student Aid Administration account totaled $1,812,000,000, with $1,281,281,000 allocated for Salaries and Expenses and $530,719,000 for Servicing Activities5.

The latest CBO projections highlight a dramatic shift in the financial outlook for the federal student loan program. What was once projected to be a profitable government investment has transformed into a significant fiscal liability, with taxpayers expected to lose hundreds of billions of dollars over the next decade.

This transformation raises important questions about the sustainability of current policies and the potential need for reforms to address growing costs. The substantial operational budget of FSA ($2.1 billion annually) adds to the overall fiscal impact of federal student aid programs.

As policymakers consider the future of federal student aid, they will need to grapple with balancing access to higher education with fiscal responsibility and ensuring that federal resources are allocated efficiently and effectively.

What happens now with the US Department of Education now that Elon Musk claims that it no longer exists? It's hard to know yet, and even more difficult after removing career government workers that we have known for years.

We are saddened to hear of contacts we know who have been fired: hard working and capable people, in an agency that has been chronically understaffed and politicized.

We also worry for the hundreds of thousands of student loan debtors who have borrower defense to repayment claims against schools that systematically defrauded them--and have not yet received justice.

And what about all those FAFSA (financial aid) forms for students starting and continuing their schooling? How will they be processed in a timely manner?

The College Meltdown continues in 2020. This phenomenon is deeper than the coronavirus, the temporary closing of campuses across the US, and the cancellation of NCAA basketball's March Madness. What we are seeing in the news should be a smaller entry in the History of American Higher Education compared to larger trends and social problems that preceded the pandemic.

College and university enrollment has been declining slowly but constantly since 2011, with for-profit colleges and community colleges taking the largest hits. And it follows larger demographic trends which include a half century of increasing inequality, including "savage inequalities" in the K-12 pipeline, crushing student loan debt, decreasing social mobility and the underemployment of college graduates, smaller families, and the hollowing out of America.

There are many parts to the current Coronavirus crisis and its effects on US higher education. But they all boil down to the Trump mantra (defund, deregulate, and privatize) and the opportunity for the elites to capitalize from the crisis, as they did during and after the Great Recession.

[Image below from Wikipedia. Higher education in the US has increasingly relied on for-profit mechanisms for growth and revenues. This includes privatized housing and services and for-profit Online Program Managers (OPMs).]

Higher education is a small but significant part of the US economy, which includes much larger sectors like Health Care and Finance. While the working class will not get bailed out, these sectors likely will, with the sudden crisis used as a rationalization. The crisis of crushing student loan debt and the much larger problems related to 50 years of growing inequality may be more disruptive in the long run, but these matters continue to be ignored.

Whether the next President is Donald Trump or Joe Biden, things could get worse for working families, unless there is mass resistance--right now I don't see that happening. For the moment, many young people are responding by living with family, not going to college, and delaying child bearing. Those who do get an education are also making economic sacrifices. Some, for example are selling their bodies as Sugar Babies to get through school.

Many state economies also look bleak in the near future. Not enough in revenues and increasing Medicaid costs make investments in education difficult to do without increasing taxes or state-level debt. And it's not likely that the wealthy will be willing to pay their fair share, unless they feel economically threatened. If that happens, rich companies and rich people can just move out of state or out of the country.

Higher Education and the Student Loan Mess

In October 2019, Trump Department of Education official Wayne Johnson resigned, recognizing that student loan debt mess was worse than anyone had imagined. US higher education enrollment is supposed to be countercyclical (improving when the economy drops) , but don't bet on it without government help.

Haven't heard any rumors in months, but it should also be interesting to see if President Trump tries to unload the $1.5T in federal loans to his banking friends using an executive order. McKinsey & Company have been tasked to determine the possibilities of such a maneuver, but there is radio silence on that front.

In the education sector, I'm watching student loan servicers and private lenders Sallie Mae (SLM), Navient (NAVI), and Nelnet (NNI) closely. Student Loan Asset-Backed Securities (also known as SLABS) are also worthy of scrutiny given the low rates of student loan repayment.

History can be many things. It can be both informative and purposely deceptive. And from time to time, historical events need to be revisited if we seek the truth. We also find critical historical analysis essential when we think about US higher education and student loan debt from a People's perspective.

From 1965 to 2010, the federal government was a backstop for private student loans, Guaranteed Student Loans, also known as the FFEL loans. Annual volume of private loans skyrocketed, from $5B in 2001 to over $20B in 2008, when 14 percent of all undergraduates had one. A secondary market for private student loan debt (student loan asset-backed securities) also began to flourish. An industry group, America's Student Loan Providers (ASLP), provided political cover for private lenders.

In 2007, President George W. Bush signed the College Cost Reduction and Access Act of 2007 (HR 2669) which cut subsidies to lenders and increasing grants to students. But this did little to contain the growing mountain of student loan debt. A mountain of unrecoverable debt that was crushing millions of consumers as the US was facing an enormous economic crisis, the Great Recession.

In rereading The Student Loan Mess, we also discovered that these private entities had not only made questionable loans, some private lenders had also bribed university officials to become preferred lenders. How commonplace this student loan grift was has not been adequately explored.

As part of Health Care and Education Reconciliation Act of 2010, President Obama's takeover of the Guaranteed Student Loan program in 2010, did get attention. Ending the Guaranteed Student Loan program was supposed to save the US government $66B over an 11-year period. This rosy projection never materialized. The FFEL loans acquired by the U.S. Department of Education (ED) during the transition to the Direct Loan program are now part of the Direct Loan portfolio. The U.S. Department of Education (ED) acquired an additional $20.4 billion in face amount of FFEL loans from lenders during the transition from the FFEL program to the Direct Loan program.

The FFEL loans that were not acquired by the U.S. Department of Education (ED) during the transition to the Direct Loan program remained with the original private lenders. These loans continue to be serviced by the private lenders that issued them.

For-profit colleges, the engine for much of this bad debt, did get scrutiny, and from 2010 to 2023, their presence was reduced. But overpriced education and edugrift continued in many forms. And after a short respite from 2020 to 2024, the mountain of bad student loan debt continues to grow.

In the increasingly commodified world of higher education, the University of Phoenix and Risepoint (formerly Academic Partnerships) represent parallel tales of how private equity, political influence, and deceptive practices have shaped the online college landscape. While their paths have diverged in branding and institutional affiliation, the underlying motives and outcomes share disturbing similarities.

The University of Phoenix: A Legacy of Legal and Ethical Trouble

The University of Phoenix (UOP) has been a central player in the for-profit college boom, particularly during and after the 2000s. Under the ownership of Apollo Education Group, and later the Vistria Group, UOP has faced a relentless stream of lawsuits, regulatory scrutiny, and public outrage.

In 2019, the Federal Trade Commission (FTC) reached a $191 million settlement with UOP over allegations of deceptive advertising. UOP falsely claimed partnerships with major corporations like Microsoft, AT&T, and Twitter to entice students. The result was $50 million in restitution and $141 million in student debt relief.

But the legal troubles didn’t stop there. In 2022 and 2023, the U.S. Department of Education included UOP in a broader class action that granted $37 million in borrower defense discharges. These claims stemmed from deceptive marketing and predatory recruitment practices.

Meanwhile, in 2024, the California Attorney General settled with UOP for $4.5 million over allegations of illegally targeting military service members between 2012 and 2015. The university’s controversial relationship with the military community also led to a temporary VA suspension of GI Bill enrollments in 2020.

The legal history includes False Claims Act suits brought by whistleblowers, including former employees alleging falsified records, incentive-based recruiter pay, and exaggerated graduation and job placement statistics. In 2019, Apollo Education settled a securities fraud lawsuit for $7.4 million.

More recently, UOP has been embroiled in political controversy in Idaho. In 2023 and 2024, the Idaho Attorney General challenged the state's attempt to acquire UOP, citing Open Meetings Act violations and lack of transparency. Though a federal judge initially dismissed the suit, Idaho’s Supreme Court allowed an appeal to proceed.

Through all of this, Vistria Group—UOP’s private equity owner since 2017—has reaped massive profits. Vistria was co-founded by Marty Nesbitt, a close confidant of Barack Obama, underscoring the bipartisan political protection that shields for-profit education from lasting accountability.

Risepoint and the Online Program Management Model

Risepoint, formerly Academic Partnerships (AP), tells a similarly troubling story, albeit from the Online Program Manager (OPM) side of the education-industrial complex. Founded in 2007 by Randy Best, a well-connected Republican donor with ties to Jeb Bush, AP helped universities build online degree programs in exchange for a significant cut of tuition—sometimes up to 50%.

This tuition-share model, though legal, has raised ethical red flags. Critics argue it diverts millions in public education dollars into private hands, inflates student debt, and incentivizes aggressive, misleading recruitment. The most infamous case was the University of Texas-Arlington, which paid AP more than $178 million over five years. President Vistasp Karbhari resigned in 2020 after it was revealed he had taken international trips funded by AP.

Risepoint was acquired by Vistria Group in 2019, placing it in the same portfolio as the University of Phoenix and other education businesses. The firm’s growing influence in higher education—fueled by Democratic-aligned private equity—reflects a deeper entanglement of politics, policy, and profiteering.

In 2024, Minnesota became the first state to ban new tuition-share agreements with OPMs like Risepoint. This legislative action followed backlash from a controversial deal between Risepoint and St. Cloud State University, where critics accused the firm of extracting excessive revenue while offering questionable value.

Further pressure came from the federal level. In 2024, Senators Elizabeth Warren, Sherrod Brown, and Tina Smith issued letters to major OPMs demanding transparency about recruitment tactics and tuition-share models. The Department of Education followed in January 2025 with new guidance restricting misleading marketing by OPMs, including impersonation of university staff.

Despite this, Risepoint continued expanding. In late 2023, the company purchased Wiley’s online program business for $150 million, signaling consolidation in a turbulent industry. Yet a 2024 report showed 147 OPM-university contracts had been terminated in 2023, and new contracts fell by over 50%.

What Ties Them Together: Vistria Group

Vistria Group sits at the center of both sagas. The Chicago-based private equity firm has made education—especially online and for-profit education—a core pillar of its investment strategy. With connections to both Democratic and Republican power brokers, Vistria has deftly navigated the regulatory landscape while profiting from public education dollars.

Its ownership of the University of Phoenix and Risepoint demonstrates a clear strategy: acquire distressed or controversial education companies, clean up their public image, and extract revenue while avoiding deep reforms. Through Vistria, private equity gains access to billions in federal student aid with minimal oversight and a bipartisan shield.

The result is a higher education ecosystem where political influence, corporate profit, and public exploitation collide. And whether through online degrees from the University of Phoenix or public-private partnerships with Risepoint, students are often the ones left bearing the cost.

As scrutiny intensifies and state and federal lawmakers demand reform, the futures of Risepoint and the University of Phoenix remain uncertain. But one thing is clear: their shared story reveals how higher education has become a battleground of greed, power, and politics.

The federal government is a sh*t show right now. From ICE abductions of pro-Palestine college students to proposed cuts to Social Security and Medicaid, the Trump administration is wreaking havoc on all of our communities.

We want to take a moment and specifically talk about student debt and higher education — work that we’ve been doing for a while now. Here’s some of what we know, what we think, and what we should do:

In recent days, the Trump administration issued an executive order to dismantle the Department of Education. Legally, this cannot be done without Congress, but in practice, this means most of the staff was simply fired. We talked a little bit about what that means for student debtors in this Twitter thread. In short, this makes the student debt crisis much worse.

Shortly after that, Trump ordered the entire federal student debt portfolio — all $1.7 trillion — to be moved from the Department of Education to the Small Business Administration (SBA). The Small Business Administration is another agency within the federal government. That means our collective creditor would still be the federal government. But will this move actually happen? Will our federal student loans somehow end up privatized? There is a LOT up in the air right now, and the short answer is we don’t know exactly what will happen, but we as debtors should remain nimble so we can exercise our collective power when we need to. Moving our student debt from the Department of Education to the SBA would be 1) illegal 2) administratively and practically difficult 3) lead to possible errors with your account.

If you haven’t already, we still highly recommend going to studentaid.gov and finding your loan details and downloading and/or screenshotting your history.

The traditional infrastructure we have long suggested debtors utilize to solve problems with their student debt — the Consumer Financial Protection Bureau (CFPB), the FSA ombudsman team, etc — have either been undermined or outright destroyed. This means there are fewer and fewer ways for us, student debtors, to get answers to problems with our student debt accounts. But we shouldn’t let Congress off the hook — we should make student loans Congress’ problem. They’re elected to serve us and it’s their job to attend to your needs.

Lastly, we want to talk about what we mean when we say Free College. Student debt has ruined lives, and will continue to as long as it exists. We shouldn’t have to borrow to pay for college — in fact, we shouldn’t have to pay at all. It should be free. And that’s what we’re fighting for. But our vision for College For All doesn’t stop at tuition-free — it means ICE and cops off campus; it means paying workers, faculty and staff a living wage; it means standing up for free speech; it means ending domestic and gender based violence on campus; and it means universities that function as laboratories for democracy and learning, not as laboratories for landlords and imperialism.

On April 17th, Debt Collective is co-sponsoring the National Higher Education Day of Action to demand our vision of College For All and oppose the hell the Trump administration is causing right now. Find an event near you HERE to participate — or start an event on your own!

And THIS SATURDAY – April 5th –we’re taking to the streets with hundreds of thousands of people across the country to tell Trump and Musk “Hands Off Our Democracy!” They’re stripping America for parts, and it's up to us to put an end to their brazen power grab. This will be one of the largest mass mobilizations in recent history — and we need you in the streets with us. There are hundreds of actions planned, find one to join near you HERE.

Whatever happens in the future, we will be more likely to win if we gird ourselves with each other’s stories and experiences so we can fight together. This is why we built a debtors’ union — the only virtual factory floor for debtors. Debt acts as a discipline and keeps people from joining the struggle for things we care about — but we can increase our numbers and build power by canceling unjust debts. We all share the same creditor and we need to stay connected to one another. Forward this email to a friend or family member and tell them to join the union and our email list so we can stay connected.

When

borrowers default on their federal student loans, the U.S. Department

of Education (“Department of Education”) can collect the outstanding

balance through forced collections, including the offset of tax refunds

and Social Security benefits and the garnishment of wages. At the

beginning of the COVID-19 pandemic, the Department of Education paused

collections on defaulted federal student loans.1

This year, collections are set to resume and almost 6 million student

loan borrowers with loans in default will again be subject to the

Department of Education’s forced collection of their tax refunds, wages,

and Social Security benefits.2

Among the borrowers who are likely to experience forced collections are

an estimated 452,000 borrowers ages 62 and older with defaulted loans

who are likely receiving Social Security benefits.3

This

spotlight describes the circumstances and experiences of student loan

borrowers affected by the forced collection of Social Security benefits.4

It also describes how forced collections can push older borrowers into

poverty, undermining the purpose of the Social Security program.5

Key findings

The

number of Social Security beneficiaries experiencing forced collection

grew by more than 3,000 percent in fewer than 20 years; the count is

likely to grow as the age of student loan borrowers trends older.

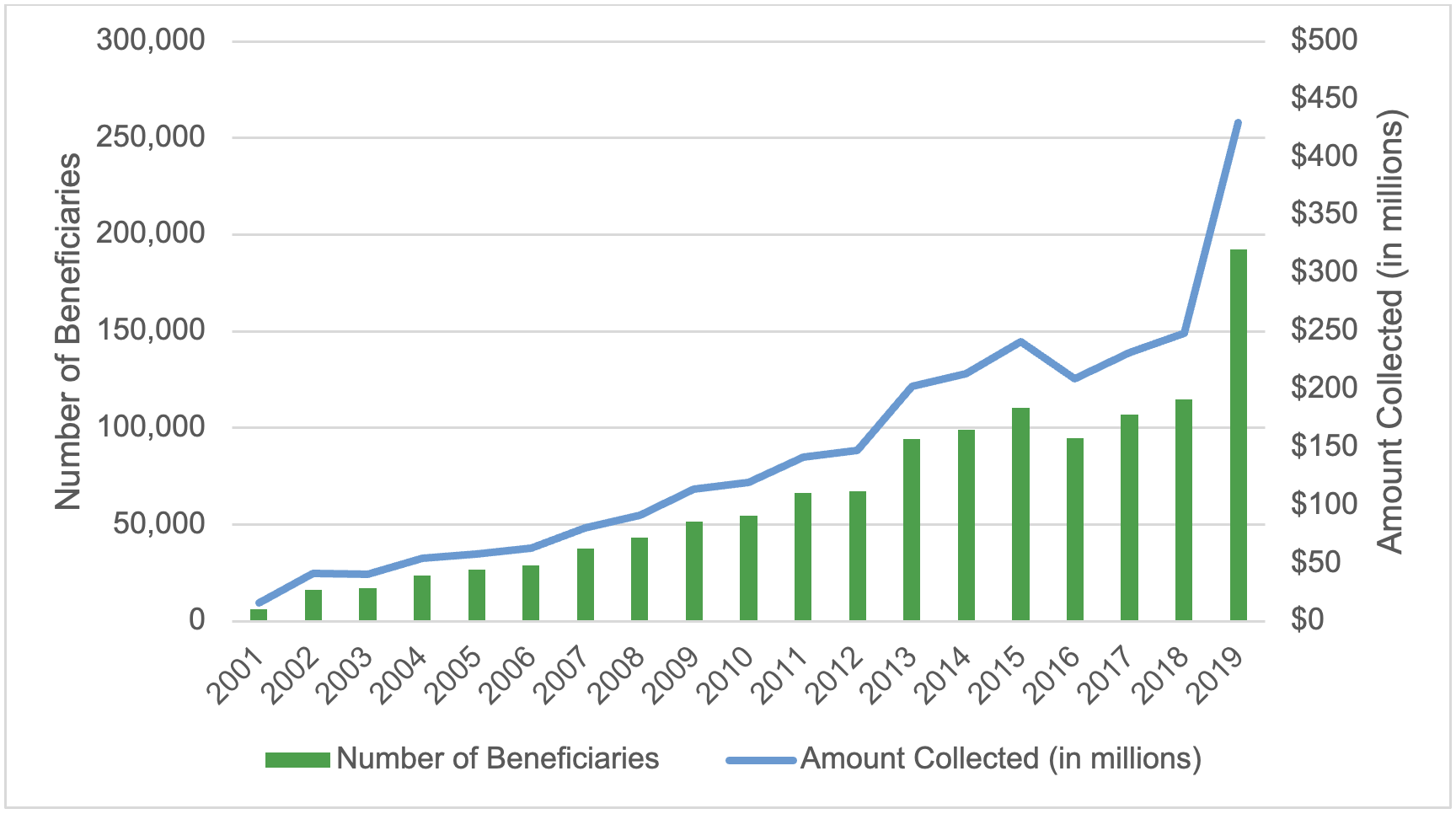

Between 2001 and 2019, the number of Social Security beneficiaries

experiencing reduced benefits due to forced collection increased from

approximately 6,200 to 192,300. This exponential growth is likely driven

by older borrowers who make up an increasingly large share of the

federal student loan portfolio. The number of student loan borrowers

ages 62 and older increased by 59 percent from 1.7 million in 2017 to

2.7 million in 2023, compared to a 1 percent decline among borrowers

under the age of 62.

The total amount

of Social Security benefits the Department of Education collected

between 2001 and 2019 through the offset program increased from $16.2

million to $429.7 million. Despite the exponential increase in

collections from Social Security, the majority of money the Department

of Education has collected has been applied to interest and fees and has

not affected borrowers’ principal amount owed. Furthermore, between

2016 and 2019, the Department of the Treasury’s fees alone accounted for

nearly 10 percent of the average borrower’s lost Social Security

benefits.

More than one in three

Social Security recipients with student loans are reliant on Social

Security payments, meaning forced collections could significantly

imperil their financial well-being. Approximately 37 percent of the

1.3 million Social Security beneficiaries with student loans rely on

modest payments, an average monthly benefit of $1,523, for 90 percent of

their income. This population is particularly vulnerable to reduction

in their benefits especially if benefits are offset year-round. In 2019,

the average annual amount collected from individual beneficiaries was

$2,232 ($186 per month).

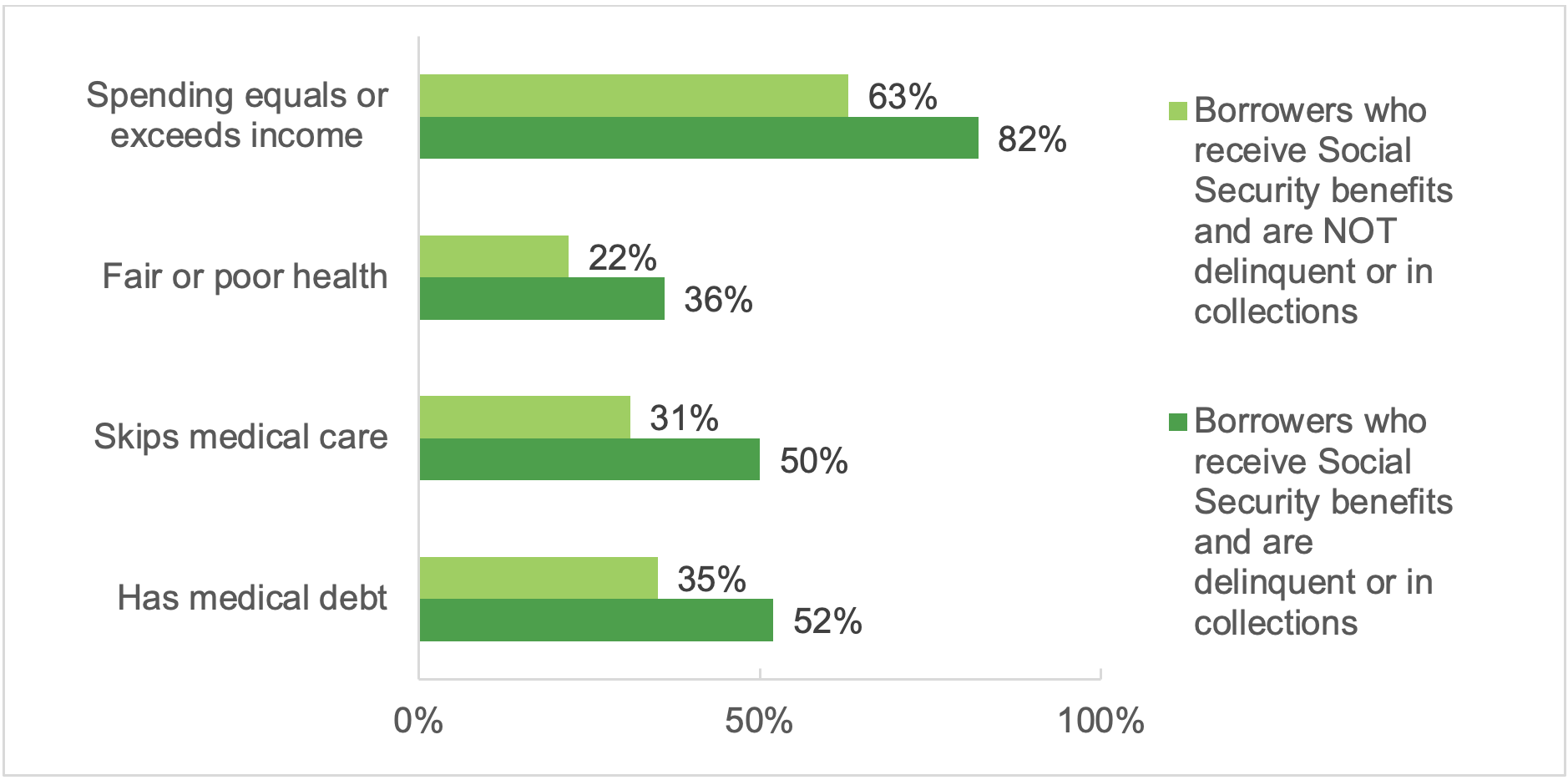

The physical well-being of half of Social Security beneficiaries with student loans in default may be at risk.

Half of Social Security beneficiaries with student loans in default and

collections skipped a doctor’s visit or did not obtain prescription

medication due to cost.

Existing minimum income protections fail to protect student loan borrowers with Social Security against financial hardship.

Currently, only $750 per month of Social Security income—an amount that

is $400 below the monthly poverty threshold for an individual and has

not been adjusted for inflation since 1996—is protected from forced

collections by statute. Even if the minimum protected income was

adjusted for inflation, beneficiaries would likely still experience

hardship, such as food insecurity and problems paying utility bills. A

higher threshold could protect borrowers against hardship more

effectively. The CFPB found that for 87 percent of student loan

borrowers who receive Social Security, their benefit amount is below 225

percent of the federal poverty level (FPL), an income level at which

people are as likely to experience material hardship as those with

incomes below the federal poverty level.

Large

shares of Social Security beneficiaries affected by forced collections

may be eligible for relief or outright loan cancellation, yet they are

unable to access these benefits, possibly due to insufficient

automation or borrowers’ cognitive and physical decline. As many as

eight in ten Social Security beneficiaries with loans in default may be

eligible to suspend or reduce forced collections due to financial

hardship. Moreover, one in five Social Security beneficiaries may be

eligible for discharge of their loans due to a disability. Yet these

individuals are not accessing such relief because the Department of

Education’s data matching process insufficiently identifies those who

may be eligible.

Taken together,

these findings suggest that the Department of Education’s forced

collections of Social Security benefits increasingly interfere with

Social Security’s longstanding purpose of protecting its beneficiaries

from poverty and financial instability.

Introduction

When

borrowers default on their federal student loans, the Department of

Education can collect the outstanding balance through forced

collections, including the offset of tax refunds and Social Security

benefits, and the garnishment of wages. At the beginning of the COVID-19

pandemic, the Department of Education paused collections on defaulted

federal student loans. This year, collections are set to resume and

almost 6 million student loan borrowers with loans in default will again

be subject to the Department of Education’s forced collection of their

tax refunds, wages, and Social Security benefits.6

Among

the borrowers who are likely to experience the Department of

Education’s renewed forced collections are an estimated 452,000

borrowers with defaulted loans who are ages 62 and older and who are

likely receiving Social Security benefits.7

Congress created the Social Security program in 1935 to provide a basic

level of income that protects insured workers and their families from

poverty due to situations including old age, widowhood, or disability.8

The Social Security Administration calls the program “one of the most

successful anti-poverty programs in our nation's history.”9

In 2022, Social Security lifted over 29 million Americans from poverty,

including retirees, disabled adults, and their spouses and dependents.10

Congress has recognized the importance of securing the value of Social

Security benefits and on several occasions has intervened to protect

them.11

This

spotlight describes the circumstances and experiences of student loan

borrowers affected by the forced collection of their Social Security

benefits.12

It also describes how the purpose of Social Security is being

increasingly undermined by the limited and deficient options the

Department of Education has to protect Social Security beneficiaries

from poverty and hardship.

The forced collection of Social Security benefits has increased exponentially.

Federal

student loans enter default after 270 days of missed payments and

transfer to the Department of Education’s default collections program

after 360 days. Borrowers with a loan in default face several

consequences: (1) their credit is negatively affected; (2) they lose

eligibility to receive federal student aid while their loans are in

default; (3) they are unable to change repayment plans and request

deferment and forbearance;13 and (4) they face forced collections of tax refunds, Social Security benefits, and wages among other payments.14

To conduct its forced collections of federal payments like tax refunds

and Social Security benefits, the Department of Education relies on a

collection service run by the U.S. Department of the Treasury called the

Treasury Offset Program.15

Between

2001 and 2019, the number of student loan borrowers facing forced

collection of their Social Security benefits increased from at least

6,200 to 192,300.16

That is a more than 3,000 percent increase in fewer than 20 years. By

comparison, the number of borrowers facing forced collections of their

tax refunds increased by about 90 percent from 1.17 million to 2.22

million during the same period.17

This exponential growth of Social Security offsets between 2001 and 2019 is likely driven by multiple factors including:

Older

borrowers accounted for an increasingly large share of the federal

student loan portfolio due to increasing average age of enrollment and

length of time in repayment. Data from the Department of Education

(which is only available since 2017), show that the number of student

loan borrowers ages 62 and older, increased 24 percent from 1.7 million

in 2017 to 2.1 million in 2019, compared to less than 1 percent among

borrowers under the age of 62.18

A larger number of borrowers, especially older borrowers, had loans in default.

Data from the Department of Education show that the number of student

loan borrowers with a defaulted loan increased by 230 percent from 3.8

million in 2006 to 8.8 million in 2019.19 Compounding these trends is the fact that older borrowers are twice as likely to have a loan in default than younger borrowers.20

Due

to these factors, the total amount of Social Security benefits the

Department of Education collected between 2001 and 2019 through the

offset program increased annually from $16.2 million to $429.7 million

(when adjusted for inflation).21

This increase occurred even though the average monthly amount the

Department of Education collected from individual beneficiaries was the

same for most years, at approximately $180 per month.22

Figure 1: Number of Social Security beneficiaries and total amount collected for student loans (2001-2019)

Source: CFPB analysis of public data from U.S. Treasury’s Fiscal Data portal. Amounts are presented in 2024 dollars.

While the total collected from

Social Security benefits has increased exponentially, the majority of

money the Department of Education collected has not been applied to

borrowers’ principal amount owed. Specifically, nearly three-quarters of

the monies the Department of Education collects through offsets is

applied to interest and fees, and not towards paying down principal

balances.23

Between 2016 and 2019, the U.S. Department of the Treasury charged the

Department of Education between $13.12 and $15.00 per Social Security

offset, or approximately between $157.44 and $180 for 12 months of

Social Security offsets per beneficiary with defaulted federal student

loans.24 As a matter of practice, the Department of Education often passes these fees on directly to borrowers.25

Furthermore, these fees accounted for nearly 10 percent of the average

monthly borrower’s lost Social Security benefits which was $183 during

this time.26

Interest and fees not only reduce beneficiaries’ monthly benefits, but

also prolong the period that beneficiaries are likely subject to forced

collections.

Forced collections are compromising Social Security beneficiaries’ financial well-being.

Forced

collection of Social Security benefits affects the financial well-being

of the most vulnerable borrowers and can exacerbate any financial and

health challenges they may already be experiencing. The CFPB’s analysis

of the Survey of Income and Program Participation (SIPP) pooled data for

2018 to 2021 finds that Social Security beneficiaries with student

loans receive an average monthly benefit of $1,524.27

The analysis also indicates that approximately 480,000 (37 percent) of

the 1.3 million beneficiaries with student loans rely on these modest

payments for 90 percent or more of their income,28

thereby making them particularly vulnerable to reduction in their

benefits especially if benefits are offset year-round. In 2019, the

average annual amount collected from individual beneficiaries was $2,232

($186 per month).29

A

recent survey from The Pew Charitable Trusts found that more than nine

in ten borrowers who reported experiencing wage garnishment or Social

Security payment offsets said that these penalties caused them financial

hardship.30

Consequently, for many, their ability to meet their basic needs,

including access to healthcare, became more difficult. According to our

analysis of the Federal Reserve’s Survey of Household Economic and

Decision-making (SHED), half of Social Security beneficiaries with

defaulted student loans skipped a doctor’s visit and/or did not obtain

prescription medication due to cost.31

Moreover, 36 percent of Social Security beneficiaries with loans in

delinquency or in collections report fair or poor health. Over half of

them have medical debt.32

Figure 2: Selected financial experiences and hardships among subgroups of loan borrowers

Source: CFPB analysis of the Federal Reserve Board Survey of Household Economic and Decision-making (2019-2023).

Social Security recipients

subject to forced collection may not be able to access key public

benefits that could help them mitigate the loss of income. This is

because Social Security beneficiaries must list the unreduced amount of

their benefits prior to collections when applying for other means-tested

benefits programs such as Social Security Insurance (SSI), Supplemental

Nutrition Assistance Program (SNAP), and the Medicare Savings Programs.33

Consequently, beneficiaries subject to forced collections must report

an inflated income relative to what they are actually receiving. As a

result, these beneficiaries may be denied public benefits that provide

food, medical care, prescription drugs, and assistance with paying for

other daily living costs.34

Consumers’

complaints submitted to the CFPB describe the hardship caused by forced

collections on borrowers reliant on Social Security benefits to pay for

essential expenses.35

Consumers often explain their difficulty paying for such expenses as

rent and medical bills. In one complaint, a consumer noted that they

were having difficulty paying their rent since their Social Security

benefit usually went to paying that expense.36

In another complaint, a caregiver described that the money was being

withheld from their mother’s Social Security, which was the only source

of income used to pay for their mother’s care at an assisted living

facility.37

As forced collections threaten the housing security and health of

Social Security beneficiaries, they also create a financial burden on

non-borrowers who help address these hardships, including family members

and caregivers.

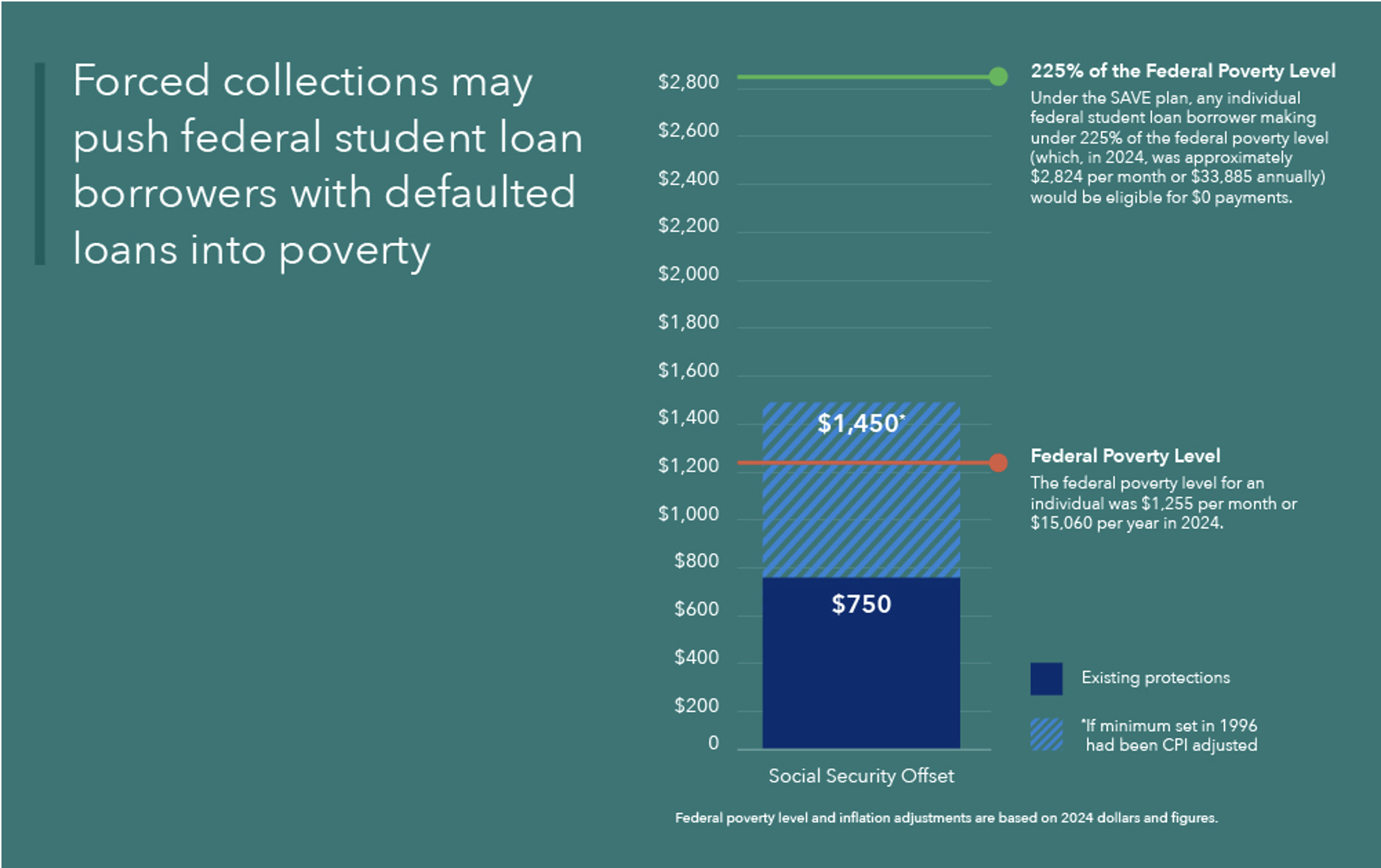

Existing minimum income protections fail to protect student loan borrowers with Social Security against financial hardship.

The

Debt Collection Improvement Act set a minimum floor of income below

which the federal government cannot offset Social Security benefits and

subsequent Treasury regulations established a cap on the percentage of

income above that floor.38

Specifically, these statutory guardrails limit collections to 15

percent of Social Security benefits above $750. The minimum threshold

was established in 1996 and has not been updated since. As a result, the

amount protected by law alone does not adequately protect beneficiaries

from financial hardship and in fact no longer protects them from

falling below the federal poverty level (FPL). In 1996, $750 was nearly

$100 above the monthly poverty threshold for an individual.39

Today that same protection is $400 below the threshold. If the

protected amount of $750 per month ($9,000 per year) set in 1996 was

adjusted for inflation, in 2024 dollars, it would total $1,450 per month

($17,400 per year).40

Figure

3: Comparison of monthly FPL threshold with the current protected

amount established in 1996 and the amount that would be protected with

inflation adjustment

Source: Calculations by the CFPB. Notes: Inflation adjustments based on the consumer price index (CPI).

Even if the minimum protected

income of $750 is adjusted for inflation, beneficiaries will likely

still experience hardship as a result of their reduced benefits.

Consumers with incomes above the poverty line also commonly experience

material hardship.41 This suggests that a threshold that is higher than the poverty level will more effectively protect against hardship.42

Indeed, in determining an income threshold for $0 payments under the

SAVE plan, the Department of Education researchers used material

hardship (defined as being unable to pay utility bills and reporting

food insecurity) as their primary metric, and found similar levels of

material hardship among those with incomes below the poverty line and

those with incomes up to 225 percent of the FPL.43

Similarly, the CFPB’s analysis of a pooled sample of SIPP respondents

finds the same levels of material hardship for Social Security

beneficiaries with student loans with incomes below 100 percent of the

FPL and those with incomes up to 225 percent of the FPL.44

The CFPB found that for 87 percent of student loan borrowers who

receive Social Security, their benefit amount is below 225 percent of

the FPL.45

Accordingly, all of those borrowers would be removed from forced

collections if the Department of Education applied the same income

metrics it established under the SAVE program to an automatic hardship

exemption program.

Existing options for relief from forced collections fail to reach older borrowers.

Borrowers

with loans in default remain eligible for certain types of loan

cancellation and relief from forced collections. However, our analysis

suggests that these programs may not be reaching many eligible

consumers. When borrowers do not benefit from these programs, their

hardship includes, but is not limited to, unnecessary losses to their

Social Security benefits and negative credit reporting.

Borrowers who become disabled after reaching full retirement age may miss out on Total and Permanent Disability

The

Total and Permanent Disability (TPD) discharge program cancels federal

student loans and effectively stops all forced collections for disabled

borrowers who meet certain requirements. After recent revisions to the

program, this form of cancelation has become common for those borrowers

with Social Security who became disabled prior to full retirement age.46 In 2016, a GAO study documented the significant barriers to TPD that Social Security beneficiaries faced.47

To address GAO’s concerns, the Department of Education in 2021 took a

series of mitigating actions, including entering into a data-matching

agreement with the Social Security Administration (SSA) to automate the

TPD eligibility determination and discharge process.48

This process was expanded further with new final rules being

implemented July 1, 2023 that expanded the categories of borrowers

eligible for automatic TPD cancellation.49 In total, these changes successfully resulted in loan cancelations for approximately 570,000 borrowers.50

However,

the automation and other regulatory changes did not significantly

change the application process for consumers who become disabled after

they reach full retirement age or who have already claimed the Social

Security retirement benefits. For these beneficiaries, because they are

already receiving retirement benefits, SSA does not need to determine

disability status. Likewise, SSA does not track disability status for

those individuals who become disabled after they start collecting their

Social Security retirement benefits.51

Consequently,

SSA does not transfer information on disability to the Department of

Education once the beneficiary begins collecting Social Security

retirement.52

These individuals therefore will not automatically get a TPD discharge

of their student loans, and they must be aware and physically and

mentally able to proactively apply for the discharge.53

The

CFPB’s analysis of the Census survey data suggests that the population

that is excluded from the TPD automation process could be substantial.

More than one in five (22 percent) Social Security beneficiaries with

student loans are receiving retirement benefits and report a disability

such as a limitation with vision, hearing, mobility, or cognition.54

People with dementia and other cognitive disabilities are among those

with the greatest risk of being excluded, since they are more likely to

be diagnosed after the age 70, which is the maximum age for claiming

retirement benefits.55

These

limitations may also help explain why older borrowers are less likely

to rehabilitate their defaulted student loans. Specifically, 11 percent

of student loan borrowers ages 50 to 59 facing forced collections

successfully rehabilitated their loans,56 while only five percent of borrowers over the age of 75 do so.57

Figure

4: Number of student loan borrowers ages 50 and older in forced

collection, borrowers who signed a rehabilitation agreement, and

borrowers who successfully rehabilitated a loan by selected age groups

Age Group

Number of Borrowers in Offset

Number of Borrowers Who Signed a Rehabilitation Agreement

Percent of Borrowers Who Signed a Rehabilitation Agreement

Number of Borrowers Successfully Rehabilitated

Percent of Borrowers who Successfully Rehabilitated

50 to 59

265,200

50,800

14%

38,400

11%

60 to 74

184,900

24,100

11%

18,500

8%

75 and older

15,800

1,000

6%

800

5%

Source: CFPB analysis of data provided by the Department of Education.

Shifting demographics of

student loan borrowers suggest that the current automation process may

become less effective to protect Social Security benefits from forced

collections as more and more older adults have student loan debt. The

fastest growing segment of student loan borrowers are adults ages 62 and

older. These individuals are generally eligible for retirement

benefits, not disability benefits, because they cannot receive both

classifications at the same time. Data from the Department of Education

reflect that the number of student loan borrowers ages 62 and older

increased by 59 percent from 1.7 million in 2017 to 2.7 million in 2023.

In comparison, the number of borrowers under the age of 62 remained

unchanged at 43 million in both years.58

Furthermore, additional data provided to the CFPB by the Department of

Education show that nearly 90,000 borrowers ages 81 and older hold an

average amount of $29,000 in federal student loan debt, a substantial

amount despite facing an estimated average life expectancy of less than

nine years.59

Existing exceptions to forced collections fail to protect many Social Security beneficiaries

In

addition to TPD discharge, the Department of Education offers reduction

or suspension of Social Security offset where borrowers demonstrate

financial hardship.60

To show hardship, borrowers must provide documentation of their income

and expenses, which the Department of Education then uses to make its

determination.61

Unlike the Debt Collection Improvement Act’s minimum protections, the

eligibility for hardship is based on a comparison of an individual’s

documented income and qualified expenses. If the borrower has eligible

monthly expenses that exceed or match their income, the Department of

Education then grants a financial hardship exemption.62

The

CFPB’s analysis suggests that the vast majority of Social Security

beneficiaries with student loans would qualify for a hardship

protection. According to CFPB’s analysis of the Federal Reserve Board’s

SHED, eight in ten (82 percent) of Social Security beneficiaries with

student loans in default report that their expenses equal or exceed

their income.63

Accordingly, these individuals would likely qualify for a full

suspension of forced collections. Yet the GAO found that in 2015 (when

the last data was available) less than ten percent of Social Security

beneficiaries with forced collections applied for a hardship exemption

or reduction of their offset.64

A possible reason for the low uptake rate is that many beneficiaries or

their caregivers never learn about the hardship exemption or the

possibility of a reduction in the offset amount.65

For those that do apply, only a fraction get relief. The GAO study

found that at the time of their initial offset, only about 20 percent of

Social Security beneficiaries ages 50 and older with forced collections

were approved for a financial hardship exemption or a reduction of the

offset amount if they applied.66

Conclusion

As

hundreds of thousands of student loan borrowers with loans in default

face the resumption of forced collection of their Social Security

benefits, this spotlight shows that the forced collection of Social

Security benefits causes significant hardship among affected borrowers.

The spotlight also shows that the basic income protections aimed at

preventing poverty and hardship among affected borrowers have become

increasingly ineffective over time. While the Department of Education

has made some improvements to expand access to relief options,

especially for those who initially receive Social Security due to a

disability, these improvements are insufficient to protect older adults

from the forced collection of their Social Security benefits.

Taken

together, these findings suggest that forced collections of Social

Security benefits increasingly interfere with Social Security’s

longstanding purpose of protecting its beneficiaries from poverty and

financial instability. These findings also suggest that alternative

approaches are needed to address the harm that forced collections cause

on beneficiaries and to compensate for the declining effectiveness of

existing remedies. One potential solution may be found in the Debt

Collection Improvement Act, which provides that when forced collections

“interfere substantially with or defeat the purposes of the payment

certifying agency’s program” the head of an agency may request from the

Secretary of the Treasury an exemption from forced collections.67

Given the data findings above, such a request for relief from the

Commissioner of the Social Security Administration on behalf of Social

Security beneficiaries who have defaulted student loans could be

justified. Unless the toll of forced collections on Social Security

beneficiaries is considered alongside the program’s stated goals, the

number of older adults facing these challenges is only set to grow.

Data and Methodology

To

develop this report, the CFPB relied primarily upon original analysis

of public-use data from the U.S. Census Bureau Survey of Income and

Program Participation (SIPP), the Federal Reserve Board Board’s Survey

of Household Economics and Decision-making (SHED), U.S. Department of

the Treasury, Fiscal Data portal, consumer complaints received by the

Bureau, and administrative data on borrowers in default provided by the

Department of Education. The report also leverages data and findings

from other reports, studies, and sources, and cites to these sources

accordingly. Readers should note that estimates drawn from survey data

are subject to measurement error resulting, among other things, from

reporting biases and question wording.

Survey of Income and Program Participation

The

Survey of Income and Program Participation (SIPP) is a nationally

representative survey of U.S. households conducted by the U.S. Census

Bureau. The SIPP collects data from about 20,000 households (40,000

people) per wave. The survey captures a wide range of characteristics

and information about these households and their members. The CFPB

relied on a pooled sample of responses from 2018, 2019, 2020, and 2021

waves for a total number of 17,607 responses from student loan borrowers

across all waves, including 920 respondents with student loans

receiving Social Security benefits. The CFPB’s analysis relied on the

public use data. To capture student loan debt, the survey asked to all

respondents (variable EOEDDEBT): Owed any money for student loans or

educational expenses in own name only during the reference period. To

capture receipt of Social Security benefits, the survey asked to all

respondents (variable ESSSANY): “Did ... receive Social Security

benefits for himself/herself at any time during the reference period?”

To capture amount of Social Security benefits, the survey asked to all

respondents (variable TSSSAMT): “How much did ... receive in Social

Security benefit payment in this month (1-12), prior to any deductions

for Medicare premiums?”

The

Federal Reserve Board’s Survey of Household Economics and

Decision-making (SHED) is an annual web-based survey of households. The

survey captures information about respondents’ financial situations. The

CFPB relied on a pooled sample of responses from 2019 through 2023

waves for a total number of 1,376 responses from student loan borrowers

in collection across all waves. The CFPB analysis relied on the public

use data. To capture default and collection, the survey asked all

respondents with student loans (variable SL6): “Are you behind on

payments or in collections for one or more of the student loans from

your own education?” To capture receipt of Social Security benefits, the

survey asked to all respondents (variable I0_c): “In the past 12

months, did you (and/or your spouse or partner) receive any income from

the following sources: Social Security (including old age and DI)?”